Intelligence Update

Superconductivity for power delivery

EMERGING TECHNOLOGY SERIES

This report is one of a series on emerging and potentially disruptive technologies that may be deployed in digital infrastructure. Here, Uptime Intelligence considers the use of superconductivity to enable easier power delivery from the grid to data centers.

Context

The AI boom is adding to the already-huge demand for data centers, but long delays in securing power connections are common and are slowing down the development of new data center projects significantly.

Although total grid capacity is a long-term issue, new connections are just as likely to be delayed by the need to upgrade distribution networks. Even when new equipment is available and funded, infrastructure (such as power lines and substations) can face planning obstacles.

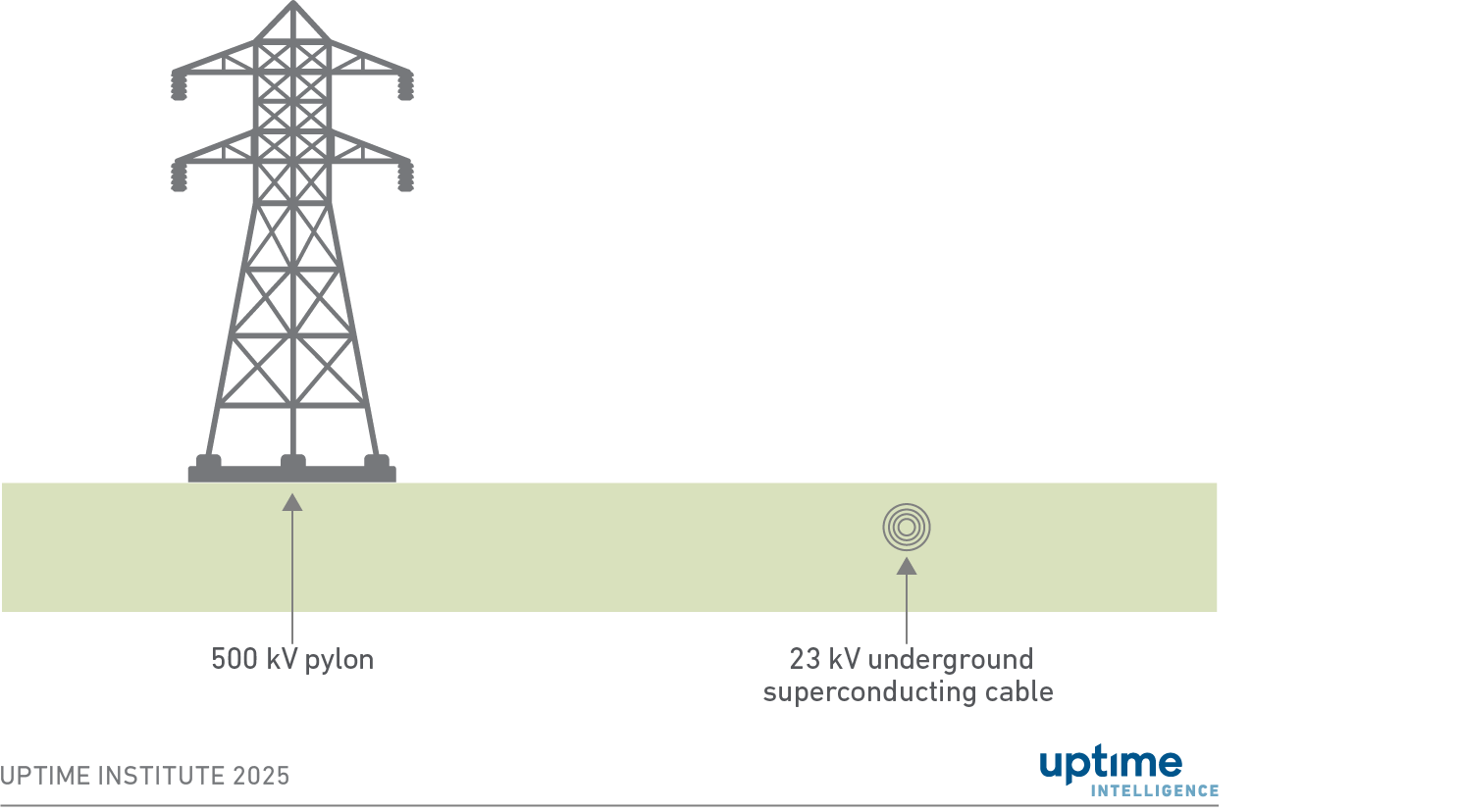

Last-mile power is delivered to the data center through high-voltage (typically ≥150 kilovolt, kV) overhead power lines, supported by transformers and substations, all of which are expensive to install and require significant land. Community groups and local authorities frequently oppose these power lines, demanding that high-voltage power distribution cables be placed underground, which would further add to costs and delays (see In the US, data center pushback is all about power).

Superconducting cables will not solve the power capacity issue, but they can contribute to a lighter-weight, more cost-effective and flexible grid. The cables are thinner, have zero electrical resistance and can carry up to 250 times the current per volume of conventional copper conductors. This means lower voltages can be used to supply the same, or more, power. Superconductive cables support distribution at medium voltage (23 kV) and can be installed underground using (sometimes already existing) conduits and cabinets instead of pylons and substations (Figure 1).

Figure 1 Superconductor cables save space and land use

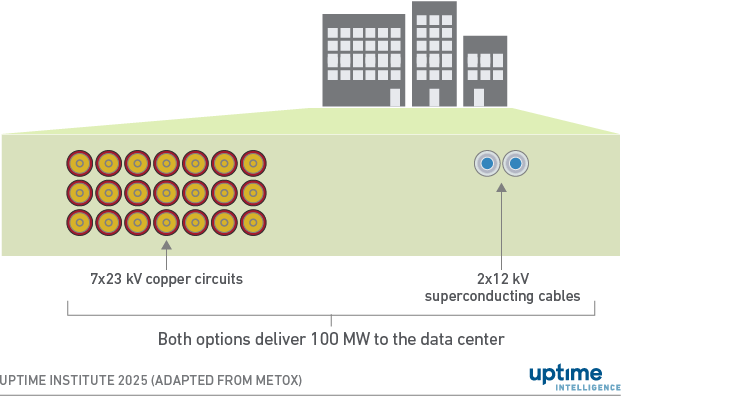

Behind-the-meter data center campuses require connections to local substations and/or microgrid power sources. Superconducting cables can reduce infrastructure, with two superconducting cables carrying the same current as 21 conventional cables (Figure 2).

Figure 2 One superconducting cable can replace multiple conventional circuits

Underground superconducting cables are likely to avoid local opposition and cut costs by minimizing space and infrastructure requirements (such as pylons) and reducing resistive heating.

But there are major drawbacks: the cables are expensive and require continuous cryogenic cooling along their entire working length. These engineering and financial challenges cast considerable doubt on their likely adoption.

The technology

Superconducting materials have no electrical resistance, delivering high currents in relatively thin cables and busbars. A superconducting cable or busbar can carry currents greater than 50 kiloamperes (kA) — a 1.2 kV connector can carry 60 MW of power.

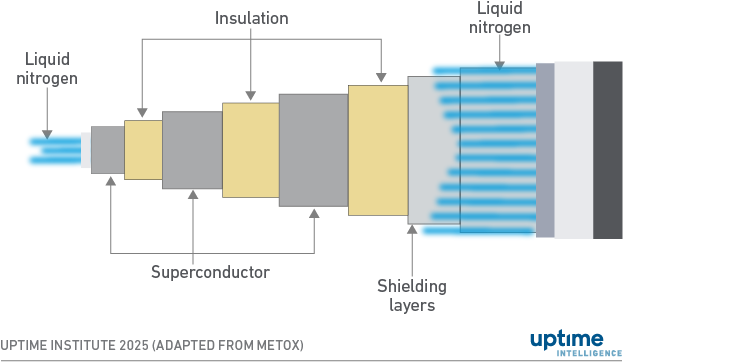

Commercial superconductivity products require the distribution of power at a low temperature of -130°C (-200°F), which is achieved by immersing the conductor in liquid nitrogen. Confusingly, these products are referred to as high-temperature superconductors (HTS) because earlier superconductors required even lower temperatures.

HTS materials typically use compounds of yttrium deposited onto metallic tapes and strengthened with layers of additional material. These tapes are wound around a central tube, along with insulator layers, shielding layers and an outer sheath to form cables (Figure 3).

Figure 3 Three-phase HTS cable design

Liquid nitrogen, generated on-site, circulates through the tube and sheath. Most systems use a closed loop, with pumps at the cable joints and a refrigeration unit in the substation. Some open loop systems require periodic topping up. Cables shorter than 5 km require a cooling station at one end; cables between 5 km and 10 km require a cooling station at each end; and longer cables need a cooling station at approximately every 5 km of cable.

HTS materials were discovered in the 1980s, but their use developed slowly until well-funded nuclear fusion startups arrived over the past decade. Only superconductor cables can carry enough current to generate the strong electromagnetic fields that prototype fusion reactors require.

In 2015, specialist providers were manufacturing a few kilometers of HTS cables each year. Today, startups such as Commonwealth Fusion Systems (US, founded in 2018) and Tokamak Energy (UK, founded in 2009), are making prototype fusion reactors which each require thousands of kilometers of HTS cable. As a result, several suppliers now provide around 10,000 km of HTS cables per year.

HTS cables are also used in particle accelerators for high-energy physics research. Lower prices will make them accessible for other applications, including power grids, wind turbines, data centers and small, efficient high-voltage transformers.

Implementations

Since 2008, several electrical utilities have successfully delivered power using HTS in at least 15 pilot projects in countries including the US, Japan, Korea, China, France and Germany. These projects connected substations in areas where congestion made conventional high-voltage connections difficult or unfeasible.

Early tests were removed from service after a demonstration period. Recent commercial projects remain in service, including substation connections in Singal, Korea (2019), and Chicago, USA (2020), and a connection at Montparnasse railway station in Paris, France (2024). The high cost of HTS cables has hindered a wider rollout. These projects have developed best practices for continuous, resilient, cryogenic cooling with a continuous nitrogen supply, reserve tanks and standby pumps.

The International Electrotechnical Commission (IEC) publishes industry standards for HTS cable systems. The International Council on Large Electric Systems (CIGRE) develops recommendations and guidelines for the design and testing of power system installations.

Economics

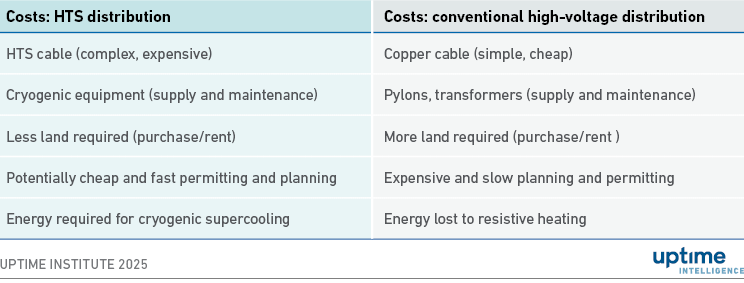

For a new technology to succeed, it does not have to be cheaper — but it certainly helps. HTS may seem exotic, but it can be more cost-effective than conventional high-voltage distribution if it delivers savings in land and infrastructure. The economic calculation will be complex and depend on factors specific to each project, including capacity, distance and congestion (see Table 1).

Table 1 Cost factors: HTS versus conventional high-voltage distribution

In most cases, power losses in conventional high-voltage cables are roughly equivalent to the cryogenic operating costs required by HTS cables. The key cost comparison comes down to the capital costs of HTS versus the permitting, land use and pylon requirements of traditional cables.

HTS power delivery is most cost-effective over short distances, because longer cable runs require higher pressure and greater temperature drops in the liquid nitrogen circulation system, adding to the cost.

Currently, the most economic range for HTS projects is between 1 km and 50 km, which is the distance where power connections to data center projects are most likely to encounter issues.

A 2017 study from the University of Bath in the UK (Economic feasibility study of using high temperature superconducting cables in UK’s electrical distribution networks) in collaboration with the UK’s National Grid compared a conventional high-voltage 132 kV link with an HTS link delivering the same power over 11 kV. While the operating costs of HTS were roughly equivalent to the cost of energy lost by the conventional solution, the higher capital costs (particularly the cable) made the HTS option 75% more expensive overall.

The cost of HTS cable is currently around $150 per kiloampere/meter (kA/m). Most analyses suggest that HTS cables will begin to replace high-voltage cables in commercial installations when the price falls below $50 per kA/m.

In 2017, HTS prices were falling consistently by 10% annually; the above study predicted that the price of a 5-km HTS link would become comparable with a conventional high-voltage cable by 2027, with shorter superconducting links becoming economic earlier.

HTS prices are falling at the anticipated rate, due to steady demand from fusion reactors. The cost of raw materials for manufacturing HTS is not considered to be a significant risk in terms of price increases because yttrium and other alternative rare-earth metals are relatively abundant.

The cryogenic system is an additional cost, but liquid nitrogen generators are well-established and support a $32 billion annual market producing 132 million tons of liquid nitrogen, used in the pharmaceutical and food industries.

Commercial activity

As the supply chain has matured, specialist superconductor suppliers have expanded. These include MetOx in the US, SuperOx in Russia (reportedly supplying Commonwealth Fusion Systems) and SuperPower in Japan (a subsidiary of Furukawa Electric that supplies Tokamak Energy).

Established superconductor cable manufacturers include NKT (Denmark), Nexans (France), LS Cable & System (South Korea) and ZMS Cable (China).

New specialty companies focusing on superconductor power delivery systems include Vision Electric Super Conductors in Germany, SuperNode in Ireland, and VEIR, which launched in the US in 2024 with $80 million from Microsoft and the UK’s National Grid.

Cryogenic systems are available from major process engineering firms such as Air Liquide (France), Air Products (UK), Linde (UK), ExxonMobil (US), and Chart Industries (US).

Drivers and barriers

Superconductivity can provide last-mile connections to the grid, as well as connections within data center campuses and microgrids.

There are several drivers for adoption:

- Last-mile superconductor grid connections use a lower voltage and do not require substations and pylons. This avoids planning delays and neutralizes community objections.

- Campus superconductors can connect multiple data centers without heavy infrastructure. Behind-the-meter implementations will be less hampered by regulation.

- Microgrid superconductors can simplify the integration of new power sources (small modular reactors, geothermal) with colocation data centers.

- HTS cables are fireproof. Nitrogen is not flammable, unlike oils used to cool conventional electrical infrastructure.

- HTS cables have a longer mean time between failures (MTBF) due to the elimination of thermal stress.

The factors slowing adoption include:

- HTS cables are still expensive, although prices are falling.

- Cryogenics add complexity

- Distribution system operators and engineering firms involved in campus development typically lack experience with HTS technology.

- Some permits may not be technology-agnostic and therefore rule out the use of superconductivity because regulators have not considered it as an option. For example, low-voltage last-mile connections may be prohibited due to safety risks associated with conventional cables. As a result, low-voltage HTS may also be restricted, despite being safer.

Maintenance and repairs will be more time consuming due to the need to warm and cool the cable.

The Uptime Intelligence View

Grid operators will increase their use of superconductors in congested grid areas as prices decrease. The next phase of deployments will target less price-sensitive niche applications, with superconductors becoming a viable option for last-mile grid connections to data centers, as well as for campus and microgrid links.

Grid regulators will need to revise permit frameworks that, in some cases, exclude superconductivity. Developers may have more flexibility to use superconductors in campuses and microgrids. However, a shortage of superconductivity skills and expertise may limit deployment.

Within five years, superconductivity is likely to become an established enabler for niche power distribution applications. Over the next decade, it could become a visible and widely adopted option for campus power distribution.

Other related reports published by Uptime Institute include:

In the US, data center pushback is all about power

Gen AI power consumption surges higher faster

About the Author

Peter Judge

Peter is a Senior Research Analyst at Uptime Intelligence. His expertise includes sustainability, energy efficiency, power and cooling in data centers. He has been a technology journalist for 30 years and has specialized in data centers for the past 10 years.

pjudge@uptimeinstitute.com